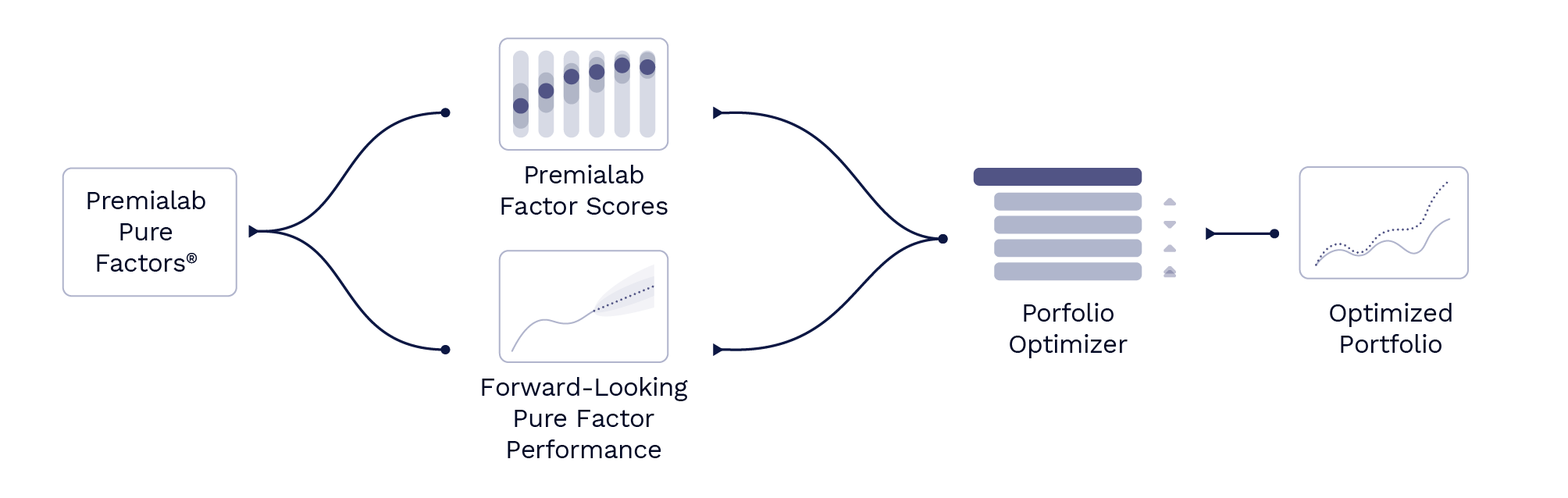

Portfolio optimization lies at the core of Quantitative Investment Strategies (QIS). In an increasingly data-driven environment, the ability to translate information into systematic portfolio tilts in a structured and efficient manner is a key source of competitive advantage.

Premialab provides a platform for systematic strategies, partnering with 18 leading index sponsors to aggregate data on over 7,000 QIS. Using this dataset, Premialab has developed proprietary Premialab Pure Factors®, designed to isolate and represent the performance of major risk premia across asset classes.

This article examines how forward-looking factor views can be incorporated into multi-factor equity portfolio construction, and discusses the implications for practitioners. Specifically, we show how combining Premialab Pure Factors® with a bottom-up factor model, implemented here using proprietary Premialab Factor Scores, yields a multi-objective optimization framework that enables dynamic tilting of equity portfolios across market regimes.