Thematic indices have witnessed increased demand over the past decade as investors recognize the potential within emerging trends, sectors, and industries. Thematic funds, being more concentrated and targeted compared to broad index funds, exhibit heightened volatility in shorter timeframes. However, over the long term, they offer the potential to capture the evolution of the chosen theme, providing differentiated and less correlated returns.

For thematic investors to strategically allocate their investments, exposure to relevant benchmarks is crucial. This paper outlines effective approaches to capitalize on the potential of thematic investments in a constantly evolving market landscape.

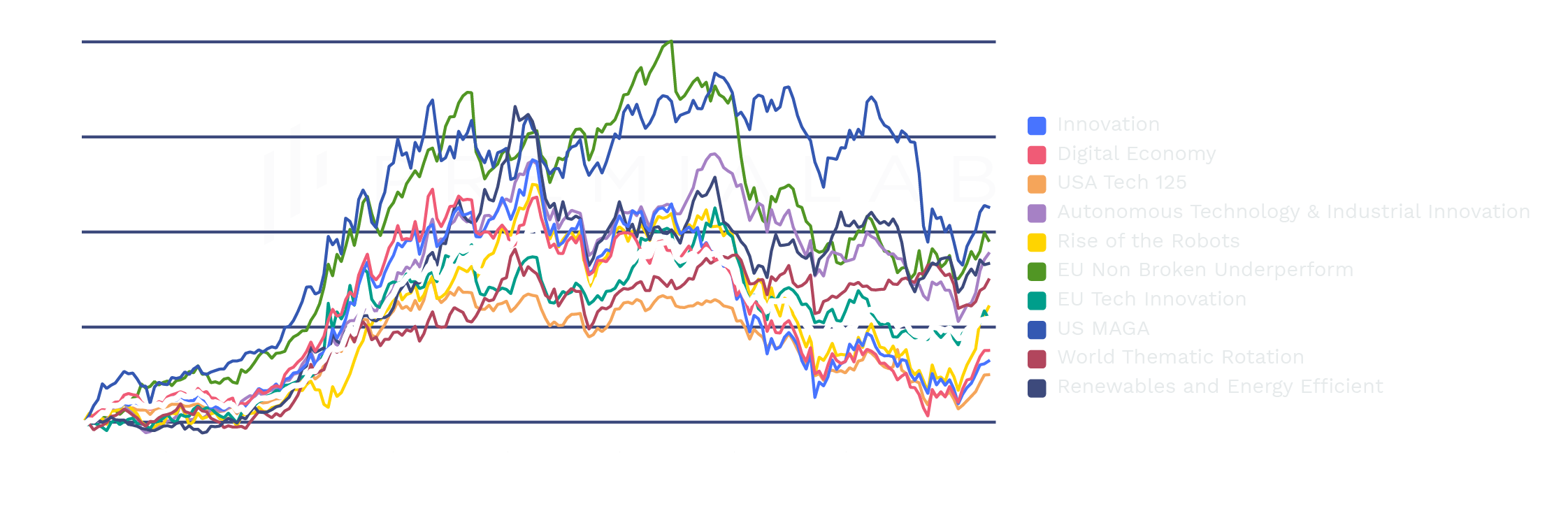

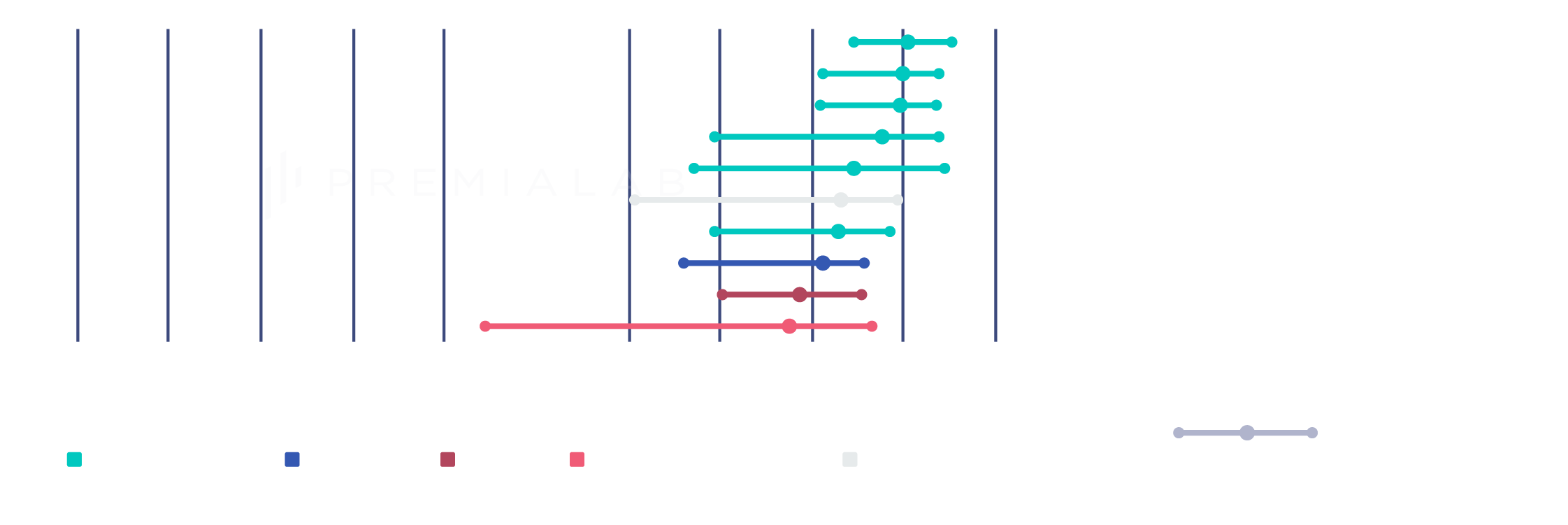

It presents methodologies for constructing and evaluating robust thematic portfolios, guiding readers through the process of conducting peer group analyses and alpha reviews to enhance portfolio outcomes. It details the strategy selection process through a meticulous and continuous search for superior portable alpha, while maintaining style consistency throughout the thematic portfolio construction. The ensuing analysis affirms that the new strategy not only outperformed its peer group but also proved to be a suitable substitute for the initial thematic strategy.

For a comprehensive understanding of the analysis and the significance of alpha in evaluating strategy performance against benchmarks, especially in thematic portfolios where opportunities from structural changes and megatrends can generate substantial alpha, refer to the full article.